Australia’s mandatory climate-related disclosures legislation passed: What you need to know

- Post Date

- 28 August 2024

- Read Time

- 7 minutes

The mandatory climate reporting Bill finally passed Parliament on 9 September. It has been a long journey to get here, but the real journey will start on 1 January 2025 when entities across the country will be required to produce climate-related disclosures.

The landmark move introduces key changes to the Corporations Act in-line with the International Sustainability Standards Board (ISSB), marking a critical evolution in how Australian companies think of and report on their climate risks and opportunities. As we welcome the changes, we also acknowledge the significant implications not just for compliance but for ensuring the future competitiveness and resilience of Australian companies.

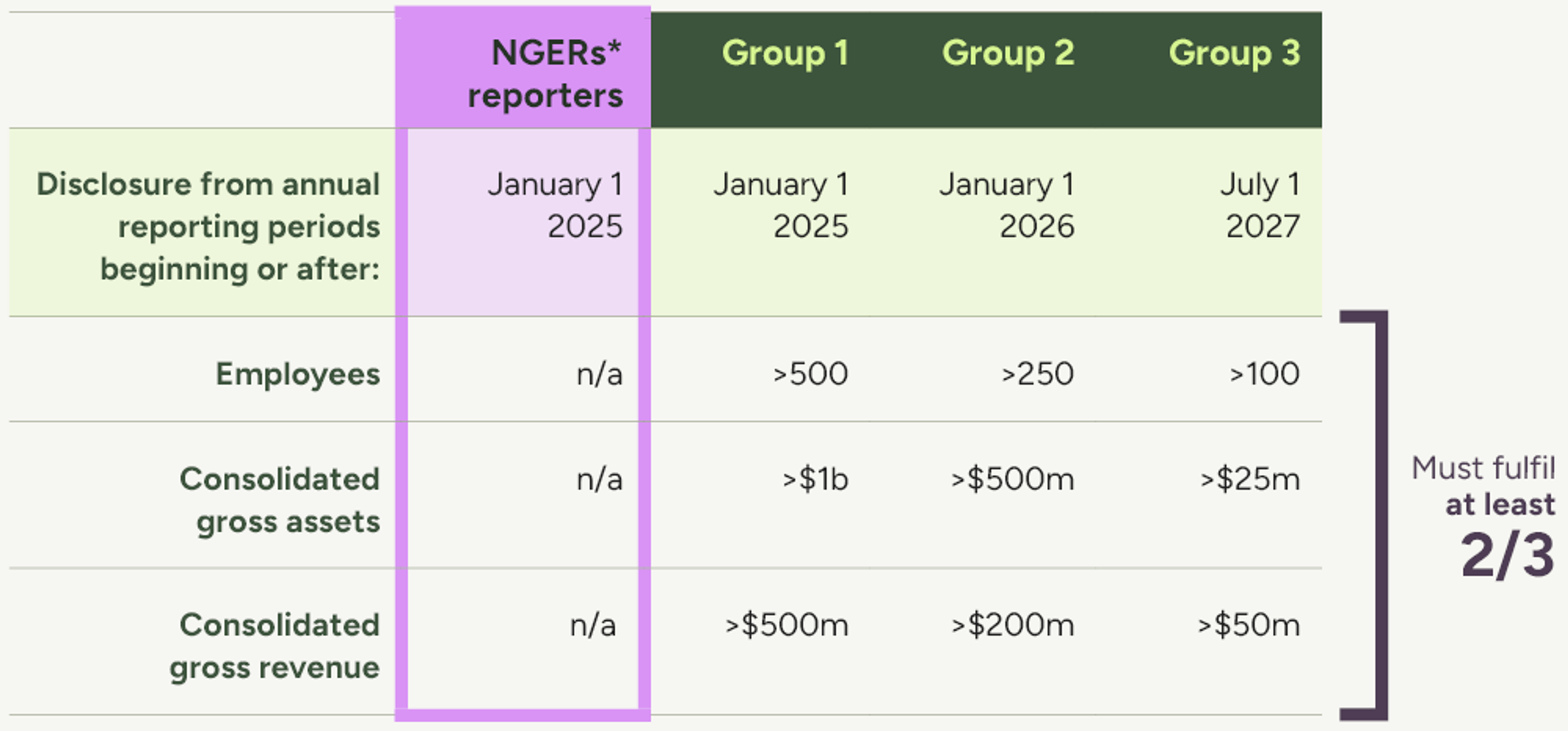

Note: Companies subject to the annual reporting requirements under the Corporations Act and emissions reporting obligations under the National Greenhouse and Energy Reporting Act 2007 (Cth) (NGER Act) will be required to disclose regardless of size.

What you need to know, in a nutshell

- Australia's new rules require companies to report on their climate risks from 1 January 2025 within a separate Sustainability Report as part of their annual reporting suite – along with the Financial Report, Directors’ Report and Audit Report.

- The new report must align with the Australian Sustainability Reporting Standards (ASRS) – which will be published by the Australian Accounting Standards Board (AASB) in its final form in the last quarter of 2024.

- For companies operating on a calendar year, this means the first disclosures will occur in or after January 2026 – for companies on a financial year, from July 2026.

- A three-year modified liability will apply for disclosures relating to scope 3 emissions, scenario analysis and transition plans. This means that for reports issued in the first three years, only the regulator will be able to bring action relating to breaches. Beyond this period, pre-existing liabilities under the Corporations Act and Australian Securities and Investments Commission Act 2001 (Cth) will apply.

- Assurance requirements similar to those in the Corporations Act 2001 will apply to climate disclosures in the new report, with reasonable assurance for all climate-related disclosures to apply from 1 July 2030.

For more details, see our factsheet.

What you can start doing today

The requirements in the proposed standards are comprehensive and will require a step-change in climate reporting for many Australian businesses. The pace and stringency of the proposed requirements will mean companies, many of whom may have not begun to look at this type of disclosure, will need to rapidly advance their climate governance, risk assessment, metrics and reporting. From our experience, there are at least four basic actions you should prioritise.

1. Take stock

To understand how well-prepared you are to respond to these proposed requirements, a good first step is to perform a readiness assessment. This means reviewing your current practices to identify gaps in data, governance, and reporting capabilities. It will help you map out where you stand against the ASRS and develop a roadmap to meet the requirements by the mandated deadlines. While the final version of ASRS has not yet been published, the draft currently available will give you a good insight into the items you need to master.

2. Integrating climate risk into governance structures

The new amendments require companies to disclose how climate-related risks and opportunities are managed and overseen at the Board and senior management levels. This is more than just a box-ticking exercise: it involves embedding climate considerations into your core business.

This will require you to ensure your leadership teams are well-informed and capable to respond to climate-related issues. Good practices include custom capability building for Board members, creating new roles or Committees dedicated to overseeing your climate strategy, management decisions and disclosures. Establishing clear accountability structures for climate-related disclosures will be crucial as you prepare to meet the new requirements.

3. Climate scenario analysis

Scenario analysis is set to become a cornerstone of climate-related financial reporting. When the Senate passed the Bill, it included an important requirement: companies must conduct climate scenario analysis using at least two climate scenarios, one consistent with the Paris Agreement, and one higher warming scenario that well exceeds 2C warming above pre-industrial levels and anticipates more severe climate impacts. These analyses will help you understand how different climate futures could affect operations, your supply chains, and financial performance.

Scenario analysis is notoriously complex so it is advisable to begin conducting these now – and not just to meet future regulatory requirements, but to better inform your strategic decision-making today. By understanding potential climate futures, you can identify risks and opportunities that may not be apparent through traditional financial analysis. This capability will also enable you to communicate more effectively with investors and other financial stakeholders, who are increasingly focused on climate resilience.

4. Emissions data

A key component of the new requirements is the disclosure of your carbon footprint – Scope 1 (direct), 2 (indirect) and 3 (indirect in your value chain). While most companies are generally comfortable and already report on Scope 1 and 2 emissions, Scope 3 can represent a bigger challenge, and it is advisable to get started sooner rather than later.

With assurance requirements for emissions data coming into effect as early as the first year of reporting[1], you must work towards complete and auditable emissions data sets, that can stand up to the same level of scrutiny as your financial data. To start, we recommend conducting an initial screening of your greatest emissions sources and developing a high-level inventory – further analysis, in particular for Scope 3 emissions, will require time and effort so it is crucial to not delay action.

A bigger picture emerges

While much of the focus around these new requirements has been on compliance, there is a significant opportunity for businesses that go beyond meeting the bare minimum. By embedding climate risk into governance, strategy and risk management, Australian companies can now position themselves as leaders. This will not only enhance their resilience to climate risks but also strengthen their appeal to financial stakeholders.

The amendments to the Corporations Act signal a new era of corporate accountability in Australia, with climate-related disclosures set to become a critical aspect of business reporting. By taking proactive steps today, you can ensure you are not only compliant but also strategically positioned for long-term success.

How SLR can help

We understand that for many companies, the new requirements can be challenging at first. We have designed our approach to help you not only navigate compliance but build your own internal capabilities from the outset. Our global team of climate experts has extensive experience supporting clients understand the nuance of the requirements and common pitfalls. Whether you are experienced in climate reporting or just getting started, SLR can support you at every step of the way.

For more information, get in touch with our experts today.

[1] Based on the Australian Auditing and Assurance Standards Board (AUASB) assurance phasing model. This is subject to change, following AUASB’s release of the proposed assurance timetable.

Recent posts

-

-

Unlocking value through solar PV repowering: A focus on module replacement and DC/AC optimisation

by David Fernandez

View post -