Australian Sustainability Reporting Standards (ASRS) – Assurance Readiness

- Post Date

- 23 November 2023

- Read Time

- 7 minutes

As of September 2024, the final standard has been confirmed with a few changes since this article was published. Please see our latest article which steps through what you need to know.

In January 2024, the Treasury released an exposure draft legislation[1] to introduce mandatory requirements for organisations to disclose their climate-related risks and opportunities. Our previous blogs and factsheet provides an overview of the disclosure requirements, and the proposed mandates covering both public and private companies, requiring the rapid implementation of climate reporting aligned with international frameworks (TCFD[2], ISSB[3]).

To understand who has to comply and when, download our factsheet

The requirements are comprehensive and will require a step-change in climate reporting for many Australian businesses. There are four key areas of disclosure which we think will be the most challenging for companies to address:

- Scope 3;

- Climate Scenario Analysis;

- Transition Planning, and

- Assurance Readiness.

While the final disclosure requirements are still subject to change, in this blog we will explore the proposed assurance requirements highlighted in the climate-related financial disclosure consultation paper, reflecting the potential evolution of the ASRS requirements and what this could mean for Australian businesses preparing for reporting.

Verification and assurance – understanding the nuances

Before delving into the specifics of the proposed assurance requirements, it’s essential to understand the two terms often discussed in this context: verification and assurance.

Verification

Verification typically involves an assessment of the processes, controls and data used in disclosing climate-related information, similar to an assurance process. While this step validates the robustness and reliability of the disclosed information, the process conducted is less extensive and does not result in an assurance opinion. Verification can take two forms – internal verification and external verification. Given the proposed alignment with the upcoming standard for assurance sustainability reporting by International Auditing and Assurance Standards Board (IAASB), conducting an internal verification in alignment with the requirements of the IAASB standards will be a crucial first step in preparing for external assurance of climate disclosures.

Assurance

The next step up from verification is assurance. Assurance typically involves an extensive review of processes, controls and data carried out by a qualified, independent professional to provide an assurance opinion. Assurance takes two forms: limited assurance and reasonable assurance.

Limited assurance is a level of assurance greater than a verification or engagements regarded as ‘agreed-upon procedures engagement’ under the Auditing and Assurance Standards Board’s (AUASB) auditing and assurance framework. The process typically involves enquiries and analytical reviews with less detailed procedures, based on an assessment of risk and materiality to support the auditor’s conclusion.

Reasonable assurance is a higher level of assurance generally involving detailed testing, evidence gathering and substantiation to support the assurance practitioner’s opinion.

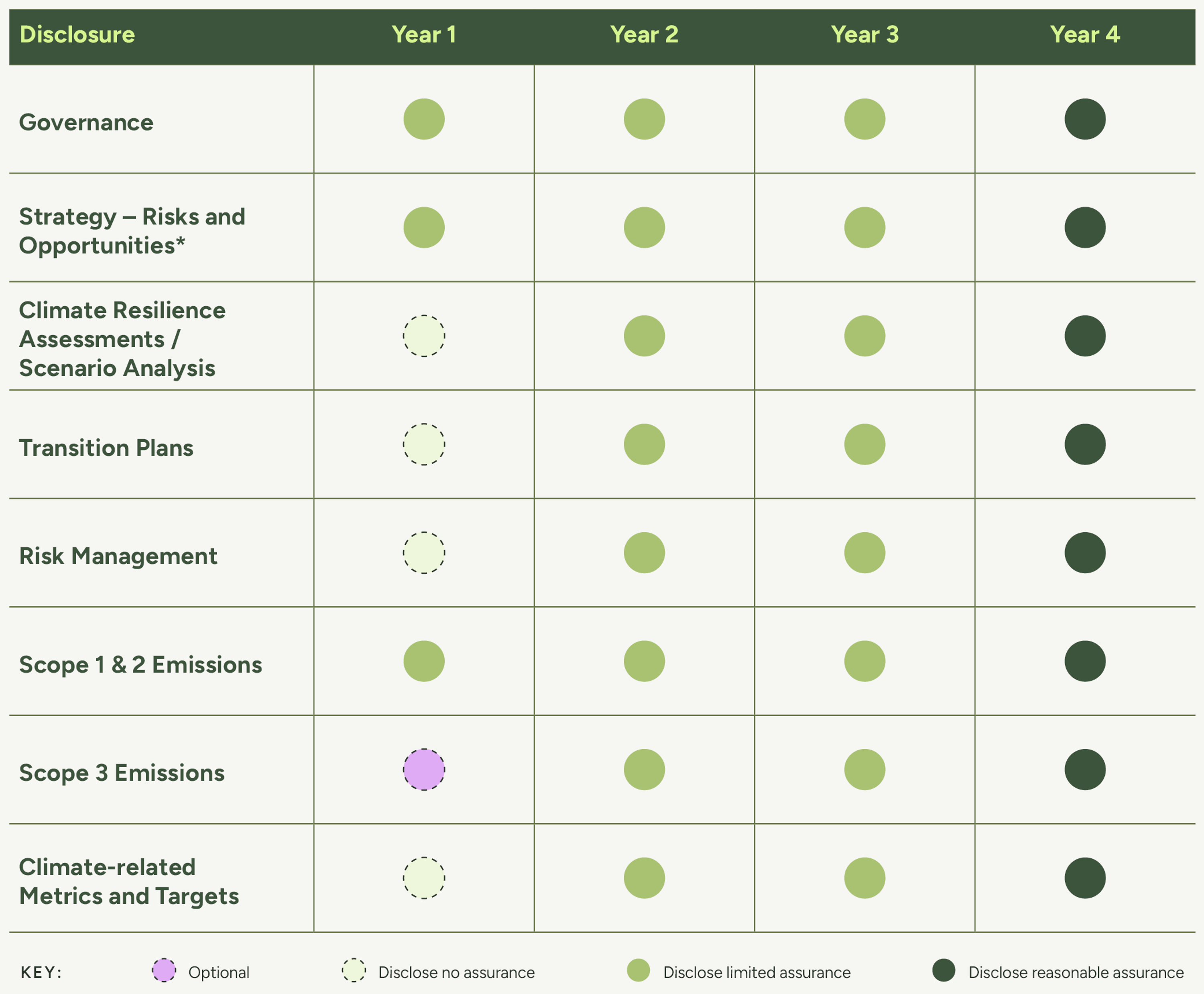

What does the consultation mention about assurance requirements?

The consultation outlines the following key points regarding assurance requirements:

- Phased approach: The proposed approach to assurance requirements is mandatory and structured over a four-year period. Depending on the specific group threshold a company falls under, this four-year period can begin as early as 2024-25.

- Scope 1, 2 and 3 emissions: Companies are initially required to have limited assurance for Scope 1, Scope 2, and Scope 3 emissions which will later be scaled up to require reasonable assurance. Given the complexities in calculating and consequently obtaining assurance on value chain emissions, assurance over Scope 3 calculation methodologies will be assured at a minimum as an interim step while companies develop capabilities and gather adequately auditable data.

- Transition plans: Assurance requirements of transition planning disclosures will involve assessing the process of determining a company’s transition plan against established-best practice. As companies progress from qualitative to quantitative transition plans, the scope of assurance requirements will increase to require reasonable assurance.

- Governance disclosures: For governance related disclosures, all companies will require reasonable assurance from the outset.

When do these requirements come into effect?

The exposure draft currently lacks specific details about assurance implementation. The assumed timelines provided below are derived from the details outlined in the consultation.

Over the four-year period of the phased approach stated in the consultation, the first year will require limited assurance of Scope 1 and 2, coupled with reasonable assurance of governance disclosures. By year 2, companies will require reasonable assurance on their Scope 1 and 2 emissions with limited assurance on Scope 3 emissions. This year will also include limited assurance of scenario analyses and transition plans, initially covering methodologies and processes before covering full quantitative assurance in year 3. At the close of this four-year timeline, all companies are required to attain reasonable assurance over all climate disclosures.

Different initial disclosure years apply to each group, but the phasing remains the same:

- Group 1: 2024/25-2027/28

- Group 2: 2026/27-2029/30

- Group 3: 2027/28-2030/31

Do these mandates carry any significant implications?

In short, yes.

As detailed in our series of ASRS blogs, the implications of the proposed ASRS framework are substantial, with major step changes in how companies will be required to manage and report on climate-related disclosures. Aligning with the proposed assurance requirements will require companies to not only calculate emissions but ensure the establishment of clear, robust and most importantly, auditable processes, systems and methodologies for calculating and reporting climate-related disclosures. As the assurance requirements continue to be updated, the importance of companies ensuring the rigour and integrity of their climate-related processes and systems cannot be overstated.

How can SLR support you?

We understand that for many companies, reporting audit-ready performance data can be challenging. We have designed our approach to climate data and disclosures to be assurance ready from the outset. Our global team of climate experts has extensive experience supporting clients through both limited and reasonable assurance of their climate disclosures, and understand the nuance, requirements and common pitfalls. Whether you are experienced in climate reporting or undertaking your footprint for the first time, SLR can support you in upgrading your disclosures and navigating audit requirements.

Webinar

We held a webinar covering the key aspects of the disclosures, case studies of best practice and practical guidance on where companies can begin addressing the requirements.

For those that were unable to attend, you can view the recording at the link below. This webinar is relevant for all companies who will be required to report, whether experienced in their disclosures or facing this for the first time.

Contact James, or Luke for further information.

Recent posts

-

-

Unlocking value through solar PV repowering: A focus on module replacement and DC/AC optimisation

by David Fernandez

View post -