Energy shocks and industrial resilience: Market dynamics and outlook

- Post Date

- 30 March 2026

- Read Time

- 16 minutes

This article sets the scene for our Energy Shocks & Industrial Resilience thought leadership series.

In this first instalment, we recap how energy markets function and the key structural differences across regions in risk exposure and price formation, before examining the current energy market shock through comparison with 2022.

In upcoming articles, we will build on this market perspective to explore the implications for industrials and identify the strategic levers available to strengthen resilience and long-term competitiveness, with dedicated deep dives for Europe and the United States.

How global energy markets transmit shocks

Global energy markets, spanning oil, gas, and electricity, have become so tightly interconnected that shocks in one part of the system rapidly ricochet across others. As a result, gas and electricity prices are increasingly sensitive to geopolitical disruptions, such as the 2026 closure of the Strait of Hormuz, damage to Qatari LNG infrastructure, or the consequences of the Nord Stream 1 & 2 sabotage earlier in the decade. Understanding how these transmission mechanisms operate is essential to interpreting current market dynamics.

From oil-linked pricing to global gas markets

Over the past two decades, gas pricing has gradually shifted from oil‑indexed contracts toward globally traded liquefied natural gas (LNG), fundamentally changing how price signals are formed and transmitted. While each market retains distinct characteristics, the expansion of global trade, particularly through LNG, has created strong transmission channels through which shocks in one segment rapidly propagate across others.

Oil remains the most globally integrated energy commodity. Benchmarks such as Brent Crude act as global reference prices, with markets responding almost instantaneously to geopolitical disruptions due to the ease of transport and high fungibility of crude. Historically, oil also played a central role in gas pricing, with long-term contracts indexed to oil products. This linkage reflected substitution between oil and gas, the absence of liquid gas markets, and widespread flaring in many producing regions, which effectively tied gas production costs to oil and made oil a convenient pricing benchmark. This association has since largely disappeared with the emergence of liquid gas hubs such as the Title Transfer Facility (TTF) and the Japan-Korea Marker (JKM), and the growth of LNG trade, which has shifted gas pricing toward its own supply–demand fundamentals.

This evolution has not reduced interdependence but rather reshaped it. Natural gas has become a globally connected market through LNG flows, with TTF and JKM serving as key, closely linked pricing hubs that respond to global factors and show correlation. LNG cargoes are redirected in response to price signals, so regional imbalances are rapidly reflected globally. As a result, gas prices are increasingly driven by global dynamics.

Europe: strong transmission of shocks to electricity markets

Electricity markets, while more local in nature, are tightly linked to fuel markets through input costs. In many European power markets, gas-fired generation often sets the marginal price of electricity under the merit-order mechanism. Under this mechanism, an increase in gas prices raises not only the cost of gas-fired generation but also the wholesale price of electricity across all generation sources, including renewables, nuclear, and hydro. Consequently, increases in gas prices - often driven by global LNG dynamics – translate directly into higher wholesale electricity prices.

Although electricity price formation remains national or zonal, Europe increasingly operates as an integrated electricity market. This reflects the progressive harmonisation of market rules, cross-border market coupling, and expanding interconnection capacity, which together enable greater price alignment across member states.

In this context, stronger market coupling means that major supply or demand shocks are transmitted more broadly across Europe, leading to a more widespread, though not fully uniform, propagation of price signals and amplifying the impact of global disruptions.

United States: more localised market dynamics

In the United States, energy market dynamics differ structurally. Electricity markets are organised around regional systems with varying market designs and generation mixes, resulting in a more localised transmission of price signals. While gas remains a key marginal fuel in several regions, its role in price formation is less uniform than in Europe.

This is primarily driven by structural factors. While the United States is a major natural gas producer and LNG exporter, abundant domestic supply and constraints on liquefaction capacity limit the ability of global price signals to affect domestic prices. As a result, the Henry Hub benchmark, which reflects domestic supply-demand dynamics, remains less sensitive to global LNG dynamics and exhibits comparatively lower volatility.

System interdependence and exposure to disruptions

Despite regional differences in price transmission, the high level of global gas market interconnection increases the system’s exposure to physical bottlenecks, particularly maritime chokepoints. The Strait of Hormuz, which facilitates the transit of a significant share of global oil and LNG supplies, is one of the most critical. Its effective closure on 2nd March 2026, following the outbreak of conflict involving Iran, combined with the attacks on regional oil and gas infrastructure such as Ras Laffan, constitutes a systemic shock to global energy markets.

Overall, the current crisis illustrates the extent to which modern energy markets function as a tightly coupled system. Oil, gas, and electricity are no longer discrete sectors but interconnected components of a global network in which disruptions cascade rapidly across markets. As a result, localised geopolitical events can translate into broad and simultaneous impacts across energy vectors.

Where current prices are vs historic and futures, and why

Recent price movements and global repricing

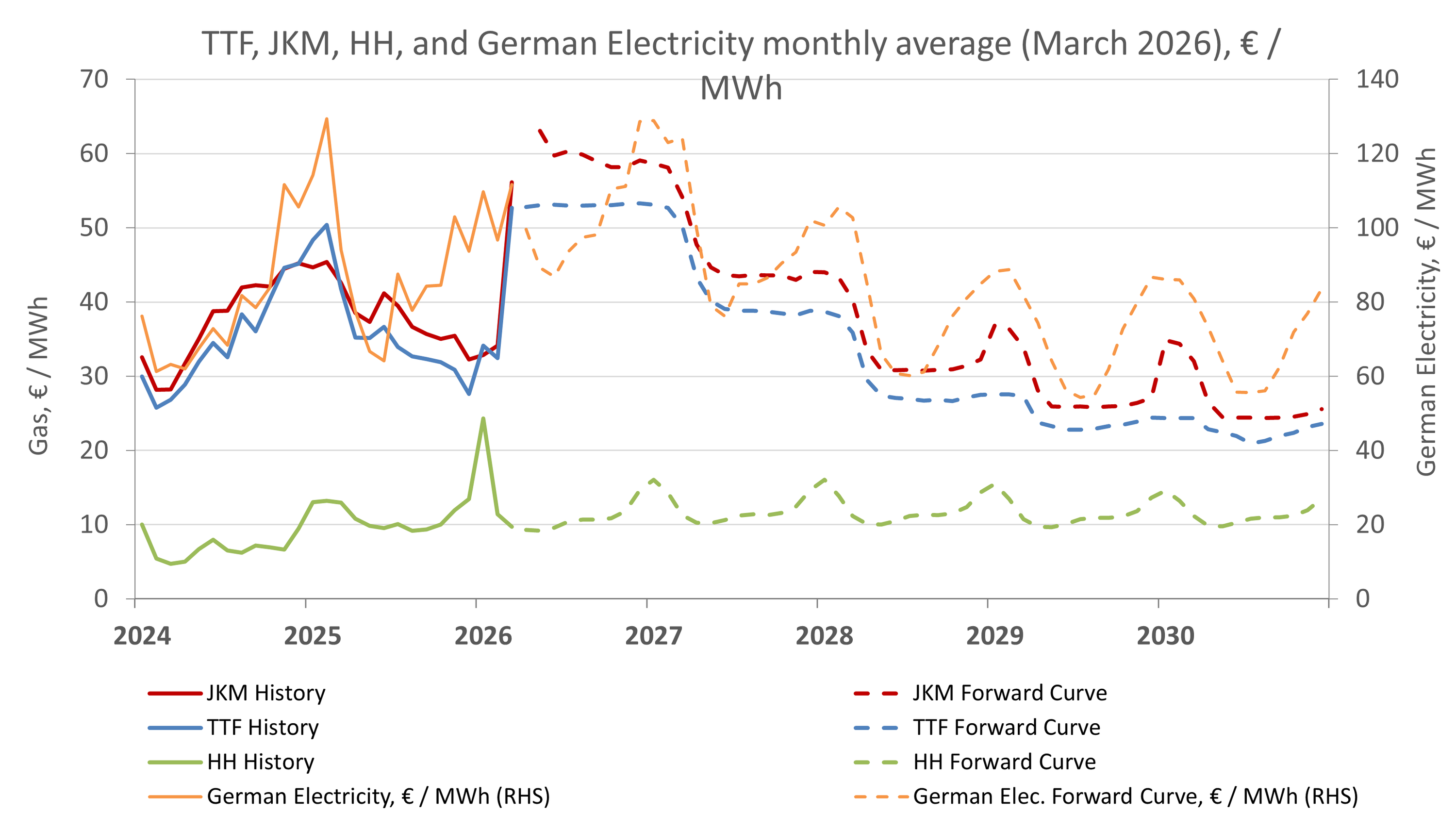

Following the outbreak of the Iran war on 28th February 2026 and the disruption of flows through the Strait of Hormuz, European gas was repriced sharply: TTF prices increased by more than 75%, rising from around €30 to approximately €55/MWh, with a further spike to around €65 / MWh following the strike on Ras Laffan on March 19th. As shown in Figure 1, this movement was closely mirrored by the JKM, reflecting the tight linkage between European and global LNG markets.

This rapid repricing reflects heightened geopolitical risk and concerns about LNG supply disruptions, as Europe and Asia compete for available cargoes. In contrast, Henry Hub prices in the United States have remained comparatively stable, reflecting the more limited linkage between global LNG prices and US domestic gas prices.

Consistent with the market dynamics described in Section 1, Figure 1 also shows a close correlation between gas and wholesale electricity prices, most clearly visible in German forward power prices, which serve as a European reference.

The 2022 European gas crisis as a benchmark

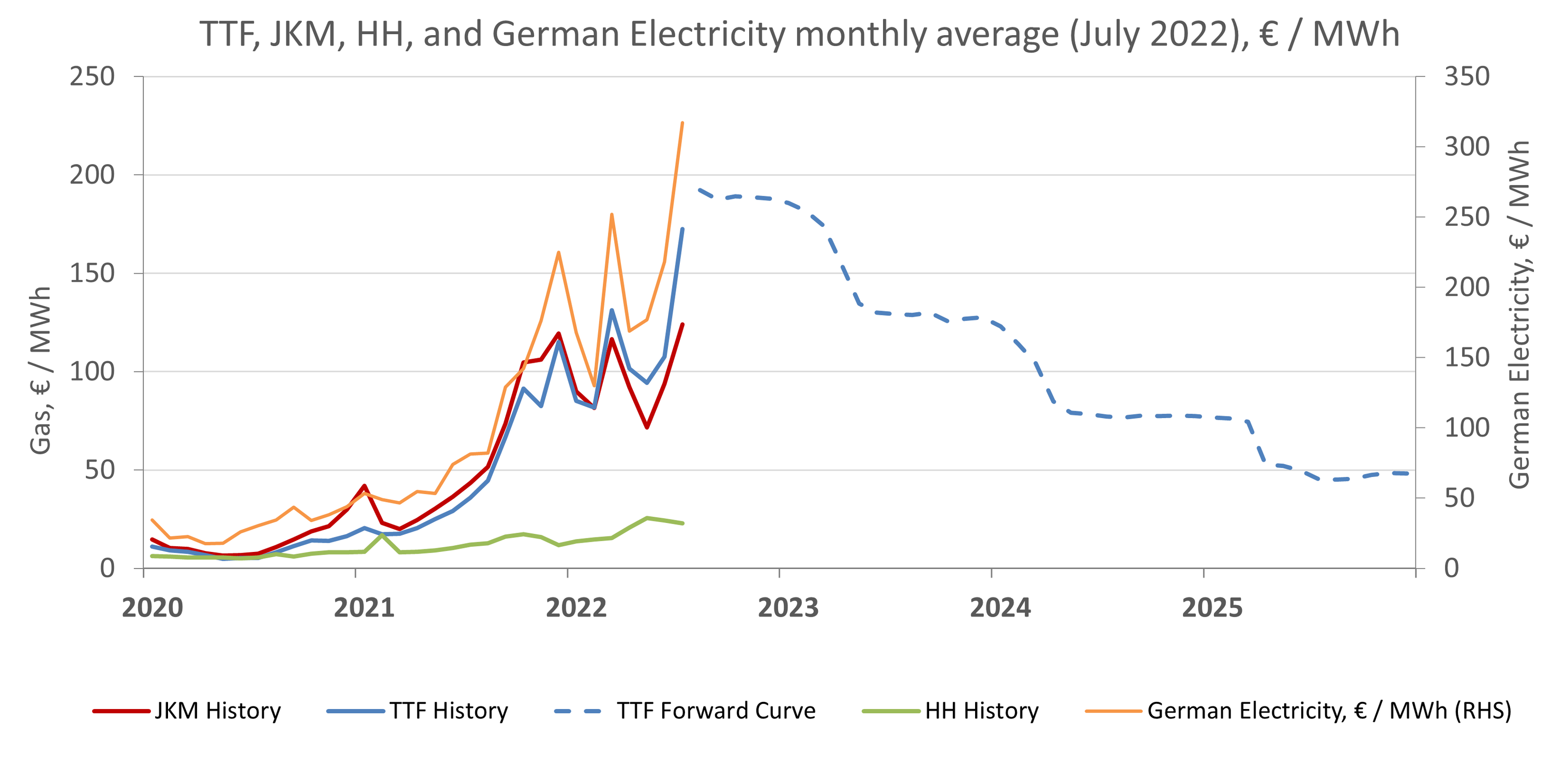

The 2022 European energy crisis provides a useful benchmark to put current developments into perspective. As shown in Figure 2, the situation in mid-2022 reflected a fundamentally different type of shock. The sharp reduction in Russian pipeline gas exports to Europe led to a structural and sustained repricing of gas markets, with TTF prices surging above €200/MWh, compared with an average of around €20/MWh in the first half of 2021, and electricity prices across the EU rose to unprecedented levels, reaching up to €580/MWh.

From 2024 to early 2026, European gas prices moderated to a range of approximately €30–50/MWh (TTF), but remained structurally elevated relative to the US, where prices stayed closer to €10/MWh (HH). This persistent differential reflected the lasting impact of the loss of Russian pipeline supply and Europe’s continued reliance on LNG.

Structural changes and improved gas market resilience since 2022

In 2022, Europe entered the gas crisis in a position of acute vulnerability. Prior to the invasion of Ukraine, the EU relied on Russia for around 40% of its gas supply, with limited diversification options. Gas storage levels were low, and Europe had insufficient LNG import capacity to rapidly replace lost pipeline volumes. As a result, the sudden reduction in Russian gas flows triggered intense competition for LNG cargoes, forcing European buyers to outbid Asian markets, amplifying price volatility and leading to a prolonged, structural repricing of gas markets.

Since then, Europe has undertaken a series of structural adjustments that have materially strengthened its resilience. Coordinated action at the EU level has played a central role, notably through joint LNG procurement, binding storage obligations, and demand‑reduction measures. LNG import capacity has expanded significantly, primarily through the rapid deployment of floating storage and regasification units (FSRUs), which accounted for around 45% of European gas imports in 2025. In parallel, pipeline diversification has progressed, with Norway supplying roughly 30% of EU gas demand in 2025.

On the demand side, European gas consumption has declined by approximately 16% compared with pre‑2022 levels, driven by a combination of behavioural changes, efficiency improvements, and industrial fuel switching. Together with higher and more systematically managed storage levels, these changes have reduced the risk of acute shortages and dampened the feedback loop between supply concerns and panic‑driven price escalation, albeit at the cost of greater exposure to global LNG pricing and structurally higher average gas prices than under the pre‑2022 pipeline‑based supply model.

As a result, while the current Middle East‑driven shock has led to sharp price movements and elevated volatility, it has not so far triggered the same degree of sustained market dislocation observed in 2022. Today’s gas market remains exposed to global geopolitical risk, but it operates within a more diversified, flexible, and resilient structural framework, shaping both the scale and persistence of price responses.

Forward gas curves and market expectations

This improved resilience is reinforced by broader changes in global LNG supply. Since 2021, US LNG exports have doubled, and additional US supply continues to enter the market. US LNG now accounts for approximately 70% of all European LNG imports, further diversifying Europe’s supply base and reducing reliance on any single source. Beyond the United States, significant new LNG export capacity is expected over the medium term from Qatar, Australia, Canada, Russia, Mozambique, Nigeria, and Algeria.

Looking ahead, continued expansion of US LNG export capacity could also gradually reduce the relative insulation of US gas prices, increasing the linkage between Henry Hub and global LNG markets.

While the timing and execution of these projects remain uncertain, their cumulative impact has raised expectations of a less structurally tight gas market than in 2022. This contrasts with the 2022 crisis, when forward prices remained elevated for several years, signalling prolonged tightness (see Figure 2). By comparison, current curves point to a more moderate trajectory, with near-term volatility followed by a gradual normalisation toward €20–25/MWh by 2030 (see Figure 1).

Risk factors and sensitivity of forward expectations

Against a baseline of a less structurally tight gas market than in 2022, forward expectations nevertheless remain highly sensitive to the evolution of geopolitical and market conditions. These forward expectations remain highly sensitive to the evolution of geopolitical and market conditions, with several factors that could materially shift price trajectories in either direction.

The primary upside risk to gas prices lies in further escalation of the Middle East crisis. Current forward curves indicate the market expects continued volatility over the next year; however, further escalation would likely sustain upward pressure.

On the downside, the most significant factor would be a de-escalation or ceasefire in the Middle East, which could ease supply constraints. A de-escalation in the Ukraine war could also contribute to lower prices, though its impact would likely be more limited unless it leads to a meaningful return of Russian gas supplies to Europe.

Additional downside factors include:

- A global economic slowdown reducing demand

- Increased LNG supply from regions outside the Middle East, particularly the United States

- Lower-than-expected demand in Asia (e.g. due to mild weather conditions)

- Higher European gas storage levels (currently at 29%, the lowest level since winter 2022)

Electricity markets: differentiated regional impacts

Gas market developments continue to shape electricity prices, but the strength and speed of this transmission vary significantly across regions. Unlike gas, electricity price dynamics remain more localised and influenced by additional factors such as weather conditions and grid constraints. As a result, while gas provides the primary directional signal, electricity prices exhibit greater short-term variability and regional dispersion around that signal - an effect that is also visible in Figure 1, where German forward power prices display seasonal patterns.

This dynamic was evident during the 2022 crisis, when wholesale power prices reached historically high levels across European markets before moderating in 2024-2025. The recent increase in gas prices has once again translated into higher electricity prices, with forward power prices indicating sustained elevation in the near term.

In the United States, these effects have been muted. The smaller impact of the gas price shock has generated a limited effect on the electricity costs for consumers. While some markets have experienced price increases linked to gas dynamics, the overall impact remains more contained than in Europe.

Limits of policy-driven mitigation

In response to the 2022 crisis, several policy discussions have emerged at European level, including proposals to decouple electricity prices from gas, introduce temporary price caps or revenue limits, or, more broadly, reform market design. These have been complemented by measures targeting gas markets, such as storage obligations, supply diversification, and energy demand reduction policies.

While alternative market designs could, in principle, reduce the influence of gas on electricity price formation, such reforms have historically faced significant economic, technical, and political hurdles. To date, no structural reform has fully removed the role of marginal gas-fired generation in setting prices, particularly given its importance in ensuring system balance during periods of low renewable output. Furthermore, recent policy developments indicate that the core principles of the marginal pricing (merit order) mechanism are likely to remain in place. As a result, gas-fired generation is expected to continue setting electricity prices in marginal periods, preserving the structural linkage between gas and power markets.

In the United States, policy discussions focus more on expanding infrastructure (e.g. Presidential Executive Order to “Unleash” Alaska energy resources) and improving system reliability, including the development of LNG export capacity and efforts to streamline electric grid interconnections (e.g. The “Connect the Grid Act” US Congress 2024 is a major federal initiative to avoid power issues like the ones faced in Texas in 2021 (Texas Power Crisis)).

As a result, policy priorities diverge: in the US, the focus is on infrastructure expansion and system reliability, while in Europe, efforts continue to explore market design adjustments to mitigate the impact of gas on electricity price formation.

Main takeaways

Recent developments across oil, gas, and electricity markets underline the extent to which global energy systems are now tightly interconnected. Shocks originating in one part of the system are rapidly transmitted across regions and energy vectors, even though their impact remains highly differentiated, reflecting structural differences between markets.

The current crisis also differs from the 2022 shock in its nature. While the disruption of Russian pipeline gas led to a structural and lasting repricing of European energy markets, the present situation is driven by geopolitical tensions affecting global LNG flows, resulting in potentially less persistent volatility.

At the same time, structural changes on both the demand and supply sides have reshaped the global gas balance. Europe has strengthened its resilience through supply diversification, expanded LNG import capacity, binding storage obligations, and sustained demand reduction. In parallel, the United States has significantly increased LNG export capacity, reinforcing its role as a central supplier to global markets and reshaping the dynamics of global LNG trade. Together with additional supply expected from other exporting regions, these developments have eased concerns over extreme structural tightness relative to 2022.

This shift is reflected in European forward curves, which price continued near-term volatility but a more moderate medium-term trajectory than during the 2022 crisis. However, these expectations remain highly sensitive to geopolitical developments and broader market conditions, particularly the evolution of tensions in the Middle East and the resilience of critical infrastructure.

Against this backdrop, energy price volatility is likely to remain a defining feature of the market environment. Understanding how these dynamics translate into concrete risks and how organisations can respond strategically becomes critical, a question explored in the following articles of this series.

Talk to our Energy Advisory experts to understand how your business can respond strategically to energy volatility.

Get in touch